CATEGORIES:

How Much Can a Commercial Tornado Shelter Actually Lower Your Insurance Premium?

April 16, 2026

If you recently installed a commercial tornado shelter, or you're seriously considering one, you're probably wondering whether the insurance savings are real. We are here to give you steps to capture the savings most business owners leave on the table.

The liability protection value is harder to quantify but worth acknowledging. Employers who provide a compliant tornado shelter and document its availability as part of a formal emergency action plan demonstrate due diligence that can reduce the probability of a successful negligence claim if a tornado event results in employee injury. Courts in tornado-prone states have increasingly examined whether employers took reasonable steps to protect workers from foreseeable severe weather events. A shelter is the most direct answer to that question.

The total economic losses from U.S. tornadoes have averaged approximately $10 to $15 billion annually in recent years, according to the NOAA National Centers for Environmental Information Billion-Dollar Disasters database. With insured losses representing 40% to 60% of total economic losses from tornado events, commercial insurers have a strong financial incentive to encourage the mitigation measures that reduce that exposure. Storm shelters are among the most direct and documentable of those measures, which is why the discount programs exist and why the financial case for installation has strengthened as tornado losses have increased.

A commercial tornado shelter's useful life typically runs 30 to 50 years. When you extend the annual insurance savings over that lifespan and account for the first-year tax and grant offsets, the cumulative financial return on a well-documented, commercial shelter installation in a high-risk state is not a marginal benefit. For businesses in Oklahoma, Kansas, Texas, and similar markets, the shelter frequently makes financial sense beyond its primary purpose of keeping your people safe.

The liability protection value is harder to quantify but worth acknowledging. Employers who provide a compliant tornado shelter and document its availability as part of a formal emergency action plan demonstrate due diligence that can reduce the probability of a successful negligence claim if a tornado event results in employee injury. Courts in tornado-prone states have increasingly examined whether employers took reasonable steps to protect workers from foreseeable severe weather events. A shelter is the most direct answer to that question.

The total economic losses from U.S. tornadoes have averaged approximately $10 to $15 billion annually in recent years, according to the NOAA National Centers for Environmental Information Billion-Dollar Disasters database. With insured losses representing 40% to 60% of total economic losses from tornado events, commercial insurers have a strong financial incentive to encourage the mitigation measures that reduce that exposure. Storm shelters are among the most direct and documentable of those measures, which is why the discount programs exist and why the financial case for installation has strengthened as tornado losses have increased.

A commercial tornado shelter's useful life typically runs 30 to 50 years. When you extend the annual insurance savings over that lifespan and account for the first-year tax and grant offsets, the cumulative financial return on a well-documented, commercial shelter installation in a high-risk state is not a marginal benefit. For businesses in Oklahoma, Kansas, Texas, and similar markets, the shelter frequently makes financial sense beyond its primary purpose of keeping your people safe.

Does a Commercial Tornado Shelter Lower Insurance Premiums?

Yes, a commercial storm shelter or safe room can reduce your business insurance premiums. But the discount is not automatic, it is not universal, and it does not happen without some effort on your part. Understanding those conditions up front will save you frustration and help you approach the conversation with your insurer the right way.Why Insurers Reward Storm Shelters

Insurance premiums are priced against expected losses. When a tornado shelter credibly reduces the probability that an event results in employee injuries and casualties, it supports continuity and the insurer's projected payout on your policy drops. That reduction in expected loss is the actuarial basis for a premium discount. Insurers are not doing this out of goodwill. They are responding to risk math. A commercial tornado shelter reduces bodily injury claims, lowers workers' compensation exposure, and cuts general liability risk associated with tornado events. All three of those outcomes improve an insurer's loss ratio on your account. The guidelines that matter most to underwriters are FEMA P-361 and ICC-500. FEMA P-361 is the federal agency's design and construction guidance for community and residential safe rooms. The ICC-500 standard is the International Code Council's minimum construction specification for above-ground safe rooms and storm shelters. Both standards are wind-speed-rated, typically to withstand EF5 tornado conditions, the highest category on the Enhanced Fujita scale used to classify tornado damage. When your shelter is designed and installed to meet or exceed these standards, underwriters have an objective basis for approving a discount rather than relying on your description of what was built. State building codes in tornado-prone states like Oklahoma, Kansas, and Texas increasingly reference these standards, which gives insurers operating in those states a regulatory framework for standardizing discount eligibility. According to NOAA's Storm Prediction Center, Oklahoma, Kansas, Texas, Nebraska, and South Dakota consistently rank among the top five states for tornado frequency, with the central plains experiencing hundreds of tornadoes annually. Insurers operating in those markets price that risk directly into commercial property premiums, making shelter discounts more financially meaningful in dollar terms than they would be in a lower-risk state.Why the Discount Is Not Guaranteed

Insurer participation varies significantly by state and by carrier. Admitted carriers, the insurance companies licensed to operate under state insurance department oversight, are more likely to have formal discount schedules for commercial storm shelters. Surplus lines carriers, which operate outside standard state rate-filing requirements, may or may not recognize shelter installations. In some high-risk markets, commercial property premiums already reflect elevated tornado exposure at a baseline rate, and insurers in those markets may offer smaller percentage discounts because they have less actuarial room to reduce the premium further. That said, even a modest discount on a high-exposure policy can translate to meaningful dollars annually, which we cover in the next section. Q: Does my shelter need to be FEMA compliant to qualify for an insurance discount? Not every insurer requires FEMA P-361 compliance specifically, but having it dramatically strengthens your case with underwriters. Carriers that offer formal discount schedules almost always require proof of compliance with ICC-500 or FEMA P-361 as the baseline eligibility condition. A shelter without documentation is much harder to get credited, even if the construction quality is equivalent.The Realistic Dollar Range of Premium Reductions

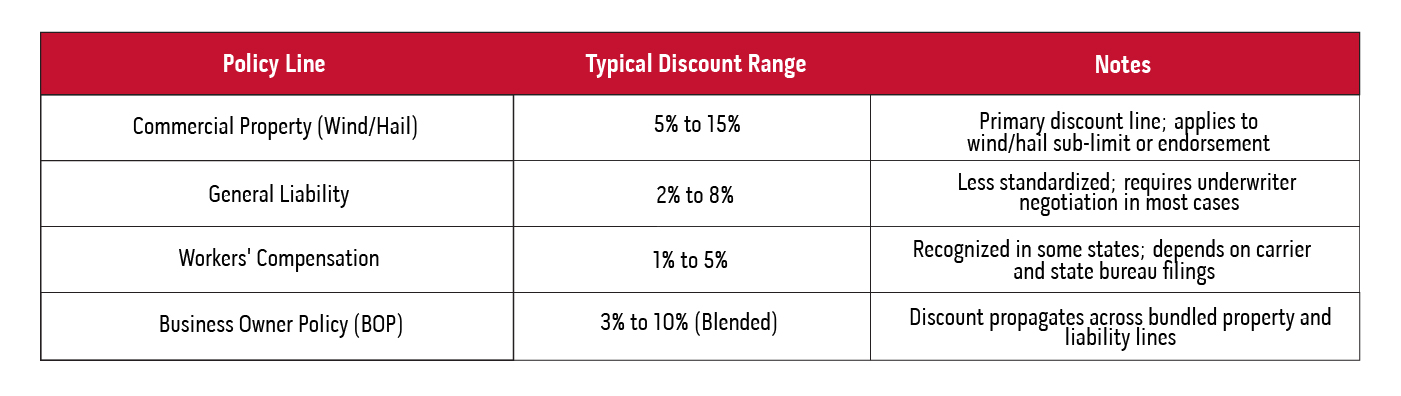

Discounts for compliant commercial tornado shelters range from roughly 2% to 15% on applicable policy lines. The wide range reflects differences in insurer guidelines, standards the shelter is built with, building type, geographic risk tier, and shelter capacity relative to your workforce. For most small to mid-size commercial properties, that translates to somewhere between $200 and $3,000 in annual premium savings, though larger commercial and industrial facilities with high wind coverage limits can see more. According to research from the Insurance Institute for Business and Home Safety (IBHS), commercial wind and hail insurance premiums in tornado-prone regions can represent a significant portion of total commercial property premiums. That proportion matters because most shelter discounts apply specifically to the wind and hail portion of your coverage, not the full policy premium. A 10% discount on a wind coverage sub-limit that represents 30% of your total premium works out to a 3% effective reduction on your overall bill. Understanding where the discount falls within your policy structure helps prevent disappointment when you see the actual savings reflected at renewal.Discount Ranges by Policy Type

What Drives the Size of Your Discount

Shelter capacity relative to your employee and occupant headcount is one of the strongest factors. A shelter sized to protect 100% of your building occupants earns a larger discount than one sized to protect 50%, because the actuarial reduction in bodily injury exposure is proportionally greater. Insurers use occupancy capacity documentation to calculate how much of their bodily injury exposure a shelter eliminates. Key Takeaway: A commercial tornado shelter built to FEMA-361 or ICC 500 standards typically reduces the wind-and-hail portion of a commercial property premium by 5% to 15%. When combined with other policy lines where the discount may apply, total annual savings of $500 to $2,500 are realistic for small- to mid-size businesses in high-risk states.Which Insurance Policies Actually Apply the Discount

The discount rarely applies to the entire commercial policy as a single blanket reduction. It targets specific lines, and knowing which ones prevents you from expecting savings that won't materialize while also ensuring you claim every credit that legitimately applies.Wind and Hail Coverage

Wind and hail coverage in a commercial property policy is the primary line of coverage where tornado shelter discounts are concentrated. In high-risk states, wind and hail coverage is often structured as a separate sub-limit or endorsement with its own premium calculation, which is where the largest percentage reductions appear. A 10% to 15% reduction on a standalone wind endorsement can range from several hundred to several thousand dollars annually, depending on your building's replacement value and location. Business interruption coverage improvements from shelter installation are indirect but real. A shelter that keeps a building structurally intact during a tornado reduces the probability of a prolonged closure that would trigger a business interruption claim. Some insurers factor this into their overall risk assessment at renewal, even if they do not publish a formal business interruption discount tied to shelter installation.Liability and Workers' Compensation Considerations

General liability and workers' compensation discounts tied to commercial storm shelters are less standardized than wind coverage discounts. They typically require direct negotiation with an underwriter rather than a straightforward credit applied from a published discount schedule. The argument to the underwriter is straightforward: a shelter reduces the probability that a tornado will cause employee injuries or third-party bodily harm on your premises, which directly lowers the insurer's expected payout on those policy lines. According to guidance from the Occupational Safety and Health Administration (OSHA), employers are required to maintain emergency action plans that address tornado events, and documented shelter availability is increasingly considered part of reasonable employer duty-of-care compliance. Presenting this compliance documentation can strengthen a workers' compensation discount request with carriers that have underwriting flexibility in that line. Q: If I have a Business Owner Policy (BOP), does the storm shelter discount apply to the whole package? Business owner policies bundle commercial property and general liability, allowing a shelter discount to apply across both coverage lines within a single BOP. The wind/hail portion of the property component usually captures the largest percentage reduction, while the general liability component may see a smaller adjustment. Ask your insurer to break out the discount by coverage component so you can see exactly where the savings land.How To Qualify for the Shelter Discount With Your Insurer

Owning a compliant shelter and actually having that reflected in your premium are two different things. The gap between them is documentation and proactive communication. Most insurers will not automatically discover your shelter installation and apply a credit. You have to ask for it, and you have to give them what they need to approve it. FEMA's guidance on shelter construction requirements is publicly available at FEMA's Safe Rooms resource page, and your shelter manufacturer or installer should have provided architect-stamped drawings at project completion. If they did not, contact the installer directly to request a copy of the compliance documentation before approaching your insurer.Required Documentation Checklist

- Architectural drawings from a licensed professional engineer that show the shelter’s location, dimensions, structural details and occupant capacity calculation. (This demonstrates the manufacturer’s compliance to FEMA P-361 or ICC-500)

- Building permit records showing the shelter installation was permitted and inspected by local authorities.

- Installation receipts or contractor invoices documenting the scope and cost of the work.

- Shelter capacity specifications showing the rated occupancy relative to your building's total occupancy.

- Manufacturer warranty documentation confirming the shelter meets or exceeds EF5 wind speed ratings.

- Third-party structural engineer inspection report, if your insurer requests independent verification.

- Photos of the installed shelter showing placement, entry points, and any posted occupancy capacity signage.

When and How To Make the Request

Policy renewal is the optimal time to submit a shelter discount request because underwriters re-price risk at each renewal and are already reviewing your account. Submit your documentation package to your agent or broker at least 30 to 60 days before your renewal date to give the underwriter time to review and apply the credit before the new policy period begins. A mid-term endorsement is also possible if your shelter was recently installed and you do not want to wait until renewal. Request a mid-term policy endorsement from your broker, submit the documentation package, and ask for a pro-rated premium adjustment. Not every carrier will process mid-term credits, but many will, especially if the installation is recent and well-documented. If your agent is unfamiliar with the shelter discount process, ask to escalate the request directly to the underwriting department. Agents who work primarily with standard personal lines policies may not be aware of the specific commercial protective device credit schedules that commercial underwriters maintain.Total ROI: Insurance Savings Plus Tax and Liability Benefits

Insurance premium savings are only one piece of the financial picture for a commercial tornado shelter investment. When you stack the available tax benefits and potential federal grant funding on top of the annual premium reduction, the total first-year financial offset can be substantial.Tax Deductions and FEMA Grant Offsets

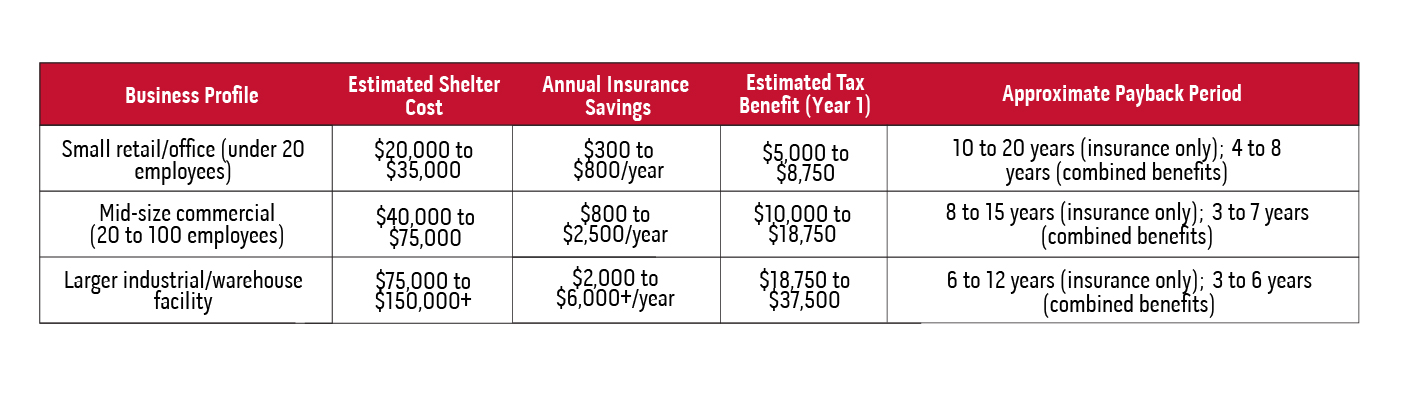

Commercial storm shelters could qualify as depreciable business property under IRS rules. Under Section 179 of the IRS tax code, businesses can deduct the full cost of qualifying capital improvements, including storm shelter installations, in the year of purchase rather than depreciating the cost over multiple years. Bonus depreciation rules available through recent tax legislation can further accelerate this deduction. On a $50,000 shelter installation, a business in the 25% effective tax bracket captures roughly $12,500 in immediate tax savings through Section 179 expensing. FEMA's Hazard Mitigation Grant Program (HMGP) and Building Resilient Infrastructure and Communities (BRIC) program have historically funded 25% to 75% of eligible safe room and storm shelter construction costs for qualifying applicants. Individual project grants through FEMA HMGP have reached up to $36,000 for residential safe rooms, with higher thresholds available for community and commercial structures. Eligibility depends on the availability of state programs, the status of post-disaster declarations, and compliance with local hazard mitigation plans. Contact your state emergency management agency to determine the current availability of HMGP or BRIC funding in your area. Commercial tornado shelter installations typically range from $20,000 to $100,000, depending on shelter size, construction type, and site preparation requirements, with below-ground shelters often running more due to excavation costs. When FEMA grant funding offsets 50% of that cost and Section 179 deductions offset another 20% to 25%, the net out-of-pocket investment before insurance savings are counted can be significantly lower than the headline installation price suggests.Payback Period Estimates by Business Size

The liability protection value is harder to quantify but worth acknowledging. Employers who provide a compliant tornado shelter and document its availability as part of a formal emergency action plan demonstrate due diligence that can reduce the probability of a successful negligence claim if a tornado event results in employee injury. Courts in tornado-prone states have increasingly examined whether employers took reasonable steps to protect workers from foreseeable severe weather events. A shelter is the most direct answer to that question.

The total economic losses from U.S. tornadoes have averaged approximately $10 to $15 billion annually in recent years, according to the NOAA National Centers for Environmental Information Billion-Dollar Disasters database. With insured losses representing 40% to 60% of total economic losses from tornado events, commercial insurers have a strong financial incentive to encourage the mitigation measures that reduce that exposure. Storm shelters are among the most direct and documentable of those measures, which is why the discount programs exist and why the financial case for installation has strengthened as tornado losses have increased.

A commercial tornado shelter's useful life typically runs 30 to 50 years. When you extend the annual insurance savings over that lifespan and account for the first-year tax and grant offsets, the cumulative financial return on a well-documented, commercial shelter installation in a high-risk state is not a marginal benefit. For businesses in Oklahoma, Kansas, Texas, and similar markets, the shelter frequently makes financial sense beyond its primary purpose of keeping your people safe.

If you’re evaluating a commercial tornado shelter—or trying to understand how it will be viewed by underwriters—talk with a shelter expert who can walk through the requirements, documentation, and real-world expectations.

Remember: the figures and discount ranges outlined in this article are based on publicly available industry data. They are intended as general reference points, not guarantees of what your specific policy will reflect. Insurance discounts vary by carrier, state, shelter type, and individual underwriting decisions. Tax benefits depend on your business structure and current tax situation. Before making any financial decisions based on this information, consult with your licensed insurance professional and a qualified tax advisor who can evaluate your specific circumstances and confirm what credits and deductions are available to you.

Frequently Asked Questions About Commercial Tornado Shelter Insurance Discounts

Are there insurance discounts for commercial tornado shelters?

Yes, many insurance companies now offer discounts for commercial properties equipped with tornado shelters, recognizing the significant risk reduction these structures provide. Installing a tornado shelter designed to meet FEMA and ICC-500 standards can reduce the likelihood of severe damage and injury during extreme weather events, which decreases claims for insurers. As a result, businesses that invest in professionally manufactured tornado shelters with designs that have undergone third-party testing often qualify for premium reductions ranging from 5% to 15%, depending on the insurer and the shelter’s specifications. Additionally, some insurers may require documentation of the shelter’s compliance with local safety standards and its accessibility to employees and customers to grant these discounts. Overall, incorporating a commercial tornado shelter not only enhances safety but can also lead to meaningful savings on insurance costs.Which insurers offer discounts for tornado shelters?

As of 2026, several leading insurance companies recognize the enhanced safety that commercial tornado shelters provide and offer discounts to policyholders who install them. Major insurers have incorporated tornado shelter discounts into their commercial property insurance policies, typically offering premium reductions of 5% to 15%. These discounts are part of broader risk mitigation programs aimed at encouraging businesses to invest in protective measures that reduce potential damage and loss during severe weather events. Additionally, some regional insurers in tornado-prone areas like Oklahoma, Texas, and Kansas offer specialized incentives for commercial properties equipped with tornado shelters that are designed to meet recognized standards like FEMA P-361 and ICC-500 standards. This reflects a growing industry trend toward rewarding proactive disaster preparedness.How much can I save with a tornado shelter discount?

With a tornado shelter discount, commercial property owners can typically save between 2% to 15% on their insurance premiums, depending on the insurer and the specific features of the shelter. Insurers recognize that tornado shelters significantly reduce the risk of injury, property damage, and business interruption during severe weather events, which translates into lower claims and overall risk exposure. For businesses located in high-risk tornado zones, these discounts can be even more substantial, sometimes reaching up to 30%, especially if the shelter meets or exceeds FEMA and ICC standards for storm protection. Check with insurers in your area to get the best available discount. Additionally, combining a tornado shelter with other safety measures like reinforced roofing and advanced warning systems may unlock further premium reductions.What qualifies a commercial tornado shelter for insurance discounts?

A commercial tornado shelter qualifies for insurance discounts primarily by meeting stringent safety and construction standards set by recognized authorities such as the International Code Council (ICC) and the Federal Emergency Management Agency (FEMA). Key qualifications include being constructed with reinforced materials capable of withstanding EF4 or higher tornado winds, having proper anchoring systems to prevent uplift, and incorporating ventilation and emergency communication features. Additionally, shelters must be strategically located on the property to ensure easy access during emergencies and comply with local building codes. Insurance providers often require documentation showing the shelter was designed and installed in accordance with recognized standards before granting discounts. These shelters significantly reduce potential damage and occupant risk, thereby lowering the insurer’s liability.Is documentation required for tornado shelter discounts?

Yes, documentation is typically required to qualify for tornado shelter discounts on commercial insurance policies. Insurers generally ask for detailed proof that the tornado shelter meets specific safety standards, such as documentation showing compliance with FEMA P-361 or ICC-500 design criteria, or confirmation the manufacturer follows the guidelines of the National Storm Shelter Association. This documentation often includes engineering reports, installation records, and compliance with local building codes to ensure the shelter provides adequate protection. Additionally, insurers may require photographs and maintenance logs to verify the shelter’s condition and accessibility. Providing thorough documentation not only helps secure the discount but also ensures that the shelter genuinely enhances safety, thereby reducing the insurer's potential claim risk.Do all types of insurance cover tornado shelter discounts?

Not all types of insurance cover tornado shelter discounts, but many commercial property and business insurance policies increasingly offer such incentives due to the proven risk reduction these shelters provide. Typically, commercial property insurance and business interruption insurance are most likely to offer discounts or premium reductions when a FEMA-compliant tornado shelter is installed on-site, as it significantly reduces potential damage and downtime risks. However, other types of insurance, such as general liability or workers’ compensation, typically do not include tornado shelter discounts since their coverage focuses on different risk areas. Business owners should consult with their insurance providers to understand specific policy terms and eligibility criteria for tornado shelter discounts, as these can vary widely by insurer and region.Can I get discounts on property insurance with a tornado shelter?

Yes, many insurance companies now offer discounts on commercial property insurance for buildings equipped with tornado shelters built to recognized standards. These shelters significantly reduce the risk of severe damage and potential injury during tornado events, which, in turn, lowers the insurer’s liability. Typically, to qualify for such discounts, the shelter must meet specific standards set by recognized organizations such as the National Storm Shelter Association (NSSA) or be constructed according to FEMA guidelines. Discounts can range from 5% to 15%, depending on the insurer and the quality of the shelter installation. Additionally, having a tornado shelter may also lead to lower premiums for business interruption coverage, as it demonstrates proactive risk mitigation.How do I apply for an insurance discount on a tornado shelter?

To apply for an insurance discount on a commercial tornado shelter, start by contacting your current insurance provider to inquire about their specific storm-safety discount programs. Most insurers require documentation proving that the shelter meets established safety standards, such as FEMA or ICC-500 guidelines. You will typically need to submit inspection reports from licensed contractors verifying that the shelter is properly installed and maintained. Additionally, some companies may request photos or a site visit to confirm compliance. Once all required documentation is submitted, your insurer will reassess your risk profile and adjust your premium accordingly, often resulting in significant savings due to the reduced risk of property damage and occupant injury from tornadoes.Are there regional differences in tornado shelter insurance discounts?

Yes, there are notable regional differences in tornado shelter insurance discounts, primarily driven by the varying frequency and severity of tornado occurrences across the country. In regions such as the Midwest and Southeast United States—often referred to as "Tornado Alley" and "Dixie Alley" respectively—insurance providers tend to offer more substantial discounts on commercial tornado shelter coverage due to the higher risk and greater demand for protective measures. These areas have seen insurers incentivize businesses to invest in robust shelters by reducing premiums by as much as 15-25%, reflecting both the increased likelihood of tornado events and the proven effectiveness of shelters in mitigating damage and liability.Do commercial buildings need certification for tornado shelter discounts?

There is no certification for tornado shelters, but commercial buildings typically need documentation demonstrating the shelter meets the applicable standards to qualify for tornado shelter discounts and reduced insurance premiums. This documentation is usually in the form of stamped architectural drawings from a licensed professional engineer. Insurance companies require that tornado shelters meet specific safety standards and building codes established by recognized authorities such as the International Code Council (ICC) or the Federal Emergency Management Agency (FEMA). This process ensures that the shelter can withstand high winds and flying debris associated with tornadoes, providing verified protection for occupants. Once verified, building owners can submit documentation to their insurance providers to receive discounts that reflect the reduced risk of injury and property damage. Therefore, obtaining proper documentation is a crucial step for commercial properties seeking tornado shelter-related insurance incentives.Author

The leading manufacturer and distributor of prefabricated steel above ground and below ground tornado shelters, and community safe rooms.

Privacy Policy | Terms Copyright ©2026 Survive-A-Storm. All rights reserved.